- This report will help the EU to steer its actions and policies in other directions where this is deemed necessary to achieve the Sustainable Development Goals (SDGs).

- This report focuses on the global dimension of the European food system, by zooming in on the trade relations between the EU and the rest of the world and the effects of this trade on local food systems.

- The report was commissioned by the SCAR Strategic Working group ARCH. We thank the members of the SCAR Working group for their valuable comments and suggestions on a draft version of this report.

The objective of this study is to enhance the knowledge on the global implications of the EU food system. In particular, the study provides:

- an analysis of the trade relations between the EU and the rest of the world from several angles (total, by geographical blocs, by income blocs and by trade agreements), with a focus on Low- and Middle-Income Countries (LMIC);

- case studies of the effects of EU trade in three products – cocoa, soy and fish - on local food systems, based on social, environmental and economic indicators;

- an explorative analysis of possible changes in the EU food system and its impact on the food systems in third countries.

Extracts:

The top 5 of imported products by the EU28 from third countries includes fish (mainly fresh salmon and frozen shrimps & prawns), fruits and nuts (bananas and almonds), coffee and tea, residues from the food industry (oil cakes from soy bean meal), and oilseeds (soy bean and rapeseed). (page 15)

The top 5 of exported products by the EU28 to third countries includes beverages (wine and spirits in particular), dairy produce and eggs (cheese), meat (pig meat), cereals (wheat), and cereal preparations (flour); Shares of this top 5 were rather stable in the period 2000-2016 apart from cereal preparations, which increased from 5% in 2000 till 8% in 2016. (page 16)

Changing demands of the European processors and retail require an adaptive response by farmers and/or other parts of the food value chain. If farmers and the food value chain are able to do so, this may result in benefits for both farming and the wider economy (through processing and packaging). However, for low- and middle-income countries the necessary transformation of their food systems presents challenges for producers, especially smallholders. Domestic barriers, like lack of access to finance, markets and transport, as well as the barriers created by standards on quality, traceability and certification, often make their participation in integrated value chains very difficult. In many countries, the ongoing fragmentation of farmland may further hinder smallholder farmers’ capacity to adopt new technologies. (page 8)

An increasing number of perspectives for assessing food systems outcomes are being developed, many aiming to provide tools to address effects of food insecurity or climate change. What is common in the majority of these novel approaches, is their emphasis on the need for a holistic and systematic interrogation of food systems. As such, a clear shift has been made from a focus on solely food production outcomes, to approaches that also incorporate food consumption, retail channels and policy incentives. (page 12)

EU-based food-related companies invest in foreign countries to either source their inputs or sell their products locally. Foreign direct investments (FDIs) are therefore also an indication of the international economic relationships among countries. In most cases FDIs and trade are complementary to each other, with FDIs generating bilateral trade. Moreover, FDIs in the food (processing, marketing) and agricultural sector may encourage trade of the country the company invested in with other foreign markets. Next, FDIs bring in knowledge and capital, contributing to the agrifood sector development in the investment receiving country. Hence, the global impact of the EU28 food systems should not be deduced only from its trade relations with third countries, yet should include all company-specific value chain activities taking place across the EU border. Such global value chain activities are not always easily traceable due to a lack of (detailed global) data on foreign direct investments in food and agriculture. Using trade data for illustrating the interconnectedness of the EU food systems with third countries is then a second best solution. (page 15)

- The production of cocoa has a serious impact on the environment. The deforestation of tropical forests and the impact of increasing use of agro-chemicals on soils and human health feature among the most researched outcomes. Smallholders in West-Africa increased their cultivated area by 3.3% annually during 1988-2007, causing 2.3m hectares of forest loss. The dominant model of full-sun cocoa farming significantly deteriorates soil quality. Another environmental risk that has the potential to negatively affect the livelihoods of cocoa farmers is climate change. A report by the International Centre for Tropical Agriculture) shows that the cocoagrowing regions in Ghana and Ivory Coast will see a temperature increase of up to 2.0 °C by 2050, resulting in a major reduction in climate suitability for coco. (page 19)

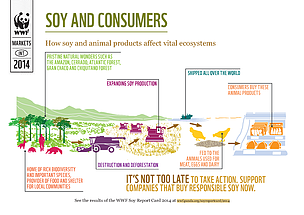

- One of the major environmental impacts of soy production is land-use change and associateddeforestation. Yearly, 3.7m hectares of forests disappear in major soy producing countries Argentina, Brazil and Paraguay. Since 2000, the soy cultivation growth area has grown by more than 10% a year in these countries. Monoculture soy production and deforestation both contribute to problems of soil degradation. Moreover, pesticide use in soy production is known to produce adverse health effects in soy producing areas. Soy production is associated with different societal impacts. In the search for new agricultural land for soy cultivation, land conflicts often arise. Soy producers are known to encroach on nature reserves and reserves for indigenous people. Mechanisation of soy production has reduced the employment opportunities in soy production, but has increased the income opportunities for farmers producing soy. Other concerns are raised about the extent to which land converted for soy production can no longer support food crops that are needed to meet the local food demand. (page 21-22)

- While the 28 EU countries capture fisheries in waters beyond the national jurisdiction of EU Member States put an excessive pressure on marine resources, there is an increasing reliance of West Africa’s coastal population on fisheries for their food and income despite decreasing total income and increasing fishing costs, which in turn aggravated poverty. Small-scale fishing in West-Africa is an activity of last resort. Despite the fact that small-scale fishing is not a source of sustainable livelihood, the number of people depending on fisheries is still increasing. Some sceptics link the loss of fisheries livelihoods to conflicts and dislocations on the African continent with migration and its accompanying environmental, economic, social and health & safety issues as a result (page 26)

More attention is needed for changes in the food consumer culture through diffusing social norms and habits regarding eating preferences or practices. Such (subtle) changes can be (secretly) cultivated by food companies, advertising and marketing, food policies or changes in the food environment (e.g. new food outlets or developments in the affordability or accessibility of particular food products). Soft values such as knowledge, environmental management, consumer preferences, even impacts on SDGs are embedded in material trade flows and financial values. In this regard, the impact of foreign direct investment (FDIs) on food systems outside the EU and the potential for sustainable finance warrants specific attention. With recognition of the cultural context to problem definition and perspectives on solutions, the commonalities and shared interests between EU and its global partners in addressing food security challenges provide a platform for mutually beneficial international collaboration in the area of food systems science and innovation. (page 36)

No comments:

Post a Comment