Achieving food security requires a rapid shift to more sustainable and resilient agriculture that remains viable in the face of economic volatility, supply chain disruptions, and increasing adverse impacts from climate change, which will exacerbate the estimated USD 260 billion investment gap that needs to be overcome to meet the targets of Sustainable Development Goal 2 (zero hunger).

We need to feed the planet using farms that can limit greenhouse gas emissions and adapt to the changing climate while protecting forests and biodiversity. And we need investors to quickly get behind this transition to make it happen.

Investors are focused on financial risks, but it is increasingly clear to many financial service providers (FSPs) that risk and sustainability profiles overlap in the agriculture sector. Simply put, a sustainable farm can yield a more sustainable return on investment and lower risks while doing more to protect people, communities, and the planet.

IISD’s State of Sustainability Initiatives (SSI) Review: Standards and Investments in Sustainable Agriculture looks at voluntary sustainability standards (VSSs) from the investor’s perspective and shows that sustainability standards can reduce financial risks and promote synergies between sound business practices and better environmental and social performance to catalyze much-needed investment in sustainable agriculture.

26 April 2022 Webinar exploring the findings (English and French)

- Cristina Larrea, IISD and report co-author

- Nathalie Bernasconi-Osterwalder, IISD

- Vivek Voora, IISD and lead report author

- Andrew Ahiaku, Aceli Africa

- Giacomo Celi, Mercon Coffee Group

- Ignacio Antequera, Global G.A.P

- Lava Bellarmin, Cooperative PAACO and the Network of Fair-Trade Cooperatives

- Marinà Herisoa Rakotoniaina, Government of Madagascar

- Representative of National Agriculture Export Development Board, Rwanda

How does VSS compliance lower financial risks for investors?

The IISD research shows that when farmers adhere to sustainability standards, their operations can become more productive and profitable and can mitigate environmental and social risks for investors. We also found that compliance helps producers build market linkages and secure contracts that they can use as collateral for financing.This report benchmarks the production criteria of 12 widely adopted VSSs against the themes of 10 popular sustainable finance frameworks. The IISD researchers also surveyed 51 FSPs active across the globe to understand how sustainability affects investment decisions. We found that, in many cases, VSS and investment criteria overlap. With standards compliance, farmers improve their practices in many ways that facilitate financing, such as by keeping detailed records; conserving water, soil, and forests; and building good relationships with workers and communities.

However, much more can be done to leverage standards to increase investment in sustainable agriculture. Accordingly, the report presents opportunities for standard-setting bodies, FSPs, and governments to leverage VSSs to attract much-needed investment in sustainable agriculture.

Access to sufficient finance for the agricultural sector has been a challenge in developing countries for decades due to perceptions of the sector’s low profitability; lack of collateral, savings, or insurance;

high risks in terms of production quality or quantity; fluctuating prices; and weather shocks. These risks are likely to increase as climate change impacts become more prominent.

An expert consultation conducted by the International Institute for Sustainable Development (IISD) in 2019 with 51 agricultural investors revealed that governance (73%), business management practices of the agribusiness (68%), and addressing climate change (56%) were perceived as highly important for reducing agricultural investment risks in developing countries (page 20)

Climate adaptation measures

- These typically include adopting practices that enable farming operations to withstand more unpredictable weather events, such as droughts or more intense precipitation events. These measures

- can include diversifying agricultural production, planting more climate-resistant varieties, and practising conservation tillage and mulching to maintain soil moisture during long droughts.

- FSPs that want to mitigate climate risks can look for agribusinesses engaging in climate adaptation efforts, such as selecting better-suited cultivars and breeds as well as preserving biodiversity and natural resources.

- The 4C, BCI, CmiA, and FSPO are the only VSSs examined that require climate adaptation activities. The Rainforest Alliance is the only standard that requires hazard emergency response plans.

VSSs operating in at least four agricultural commodity sectors— bananas, coffee, cocoa, and cotton—have captured close to 10%–15% of their respective markets by 2018

As they continue to grow in the marketplace, VSSs are expected to remain an important tool for helping the agricultural sector become more sustainable. (page 21)

VSSs have traditionally focused on internalizing the external socio-economic and environmental costs of agricultural production. Some examples of internalizing external socio-economic and environmental costs include requiring farmers to maintain soil fertility, preserve water sources, or guarantee workers’ health and safety. Consequently, incorporating production criteria in the business aspects of agricultural production has been a lower priority. (page 106)

Commodity investment profiles

The following subsections present commodity investment profiles for the banana, cocoa, coffee, cotton,

palm oil, soybean, sugarcane, and tea sectors, where VSSs in agriculture are most active. These profiles include information on market status and outlook, sustainability challenges, and investment profiles, which present a business case for investing in VSS-compliant agriculture.1. Bananas

6. Soybeans

1. Bananas

- The involvement of smallholders in banana cultivation is most relevant in LDCs where bananas are subsistence crops, often traded in local and regional markets.

- Domestic banana consumption provides nutritional and food security for around 400 million people and 25% of the daily caloric intake in many sub-Saharan countries.

- Global banana production is expected to rise at a CAGR (Compound Annual Growth Rate) of 4.1% from 2021 to 2026, with demand increasing due to population growth in developing countries, greater purchasing capacity in the Asia-Pacific region, and health concerns driving up fruit consumption in Europe and North America.

- Compared to other tropical fruits, such as mangoes and guavas, bananas have proven relatively resilient to the negative effects of COVID-19.

- Bananas are often grown on large-scale monoculture plantations with limited genetic diversity, making them vulnerable to the spread of pests and diseases This encourages farmers to rely heavily on pesticides to maintain productivity in banana plantations.

- As the development of pest-resistant cultivars has not yet been successful, farmers are limited to using harmful pesticides that can negatively impact human and ecological health, potentially leading to healthcare and environmental remediation costs as well as challenges in product marketability due to exceeding maximum residual pesticide limits (page 29)

- Investments are needed to help banana plantations become VSS compliant. For example, to comply with the GLOBALG.A.P. standard, banana plantations require infrastructure investments for handwashing and produce packing and storage facilities. These types of investments are especially needed for small banana producers with fewer resources to become VSS compliant, which can improve their access to export markets and attract investments by providing additional assurances that producers can repay loans.

2. Cocoa

- Some 40 million–50 million people depend on the cocoa sector for their livelihoods, and 5

million cocoa farmers live in extreme poverty. - Maintaining financially viable cocoa farming operations has come at the expense of social and environmental impacts in the form of labour rights infringements and deforestation.

- The business case for investing in VSS-compliant cocoa is based primarily on the growing demand for more sustainable cocoa, systemic poverty among smallholder cocoa farmers, and the significant value-addition opportunities in cocoa-producing countries. Furthermore, cocoa investments increasingly face legal and reputational risks as companies commit to sourcing their cocoa from zero-deforestation areas.

- IDH – The Sustainable Trade Initiative, could reshape the European cocoa market, as the Belgian port of Antwerp is a key entry point for cocoa imports that are eventually re-exported across Europe.

- FSPs (Finance Service Providers) can leverage profitability and socio-ecological improvements to attract more capital and business opportunities. Smallholder cocoa farmer groups in the Democratic Republic of the Congo, Ecuador, Peru, and Nicaragua selling high-quality and certified cocoa beans via direct trades with chocolate manufacturers and in lucrative bean-to-bar markets are examples of VSS-compliant production that has led to improved incomes and living conditions for smallholders.

- There are many investment opportunities for the value addition of cocoa beans in producing countries such as Madagascar, Nigeria, and Côte d’Ivoire. Mon Choco, an Ivorian chocolate manufacturer, uses West African Organic-certified cocoa beans and environmentally friendly processing practices to produce chocolate bars adapted to local tastes.

3. Coffee

- An estimated 125 million people depend on coffee for their livelihoods.

- The largest coffee-buying companies, such as the Kraft Heinz Company, The Coca-Cola

Company, Nestlé SA, JM Smucker Company, and JAB Holding Company, are sourcing more and more sustainable coffee - Although full-sun monocrop coffee systems may offer higher short-term yields and returns, they could reduce profitability in the medium to long term.

- Climate change is expected to halve the land suitable for growing Arabica coffee by 2050, threatening 60% of wild coffee and putting the world’s coffee supply at risk. For instance, Ugandan coffee production at lower altitudes (less than 1,300 m) is expected to become untenable due to mounting incidences and intensities of drought and increased pests and diseases.

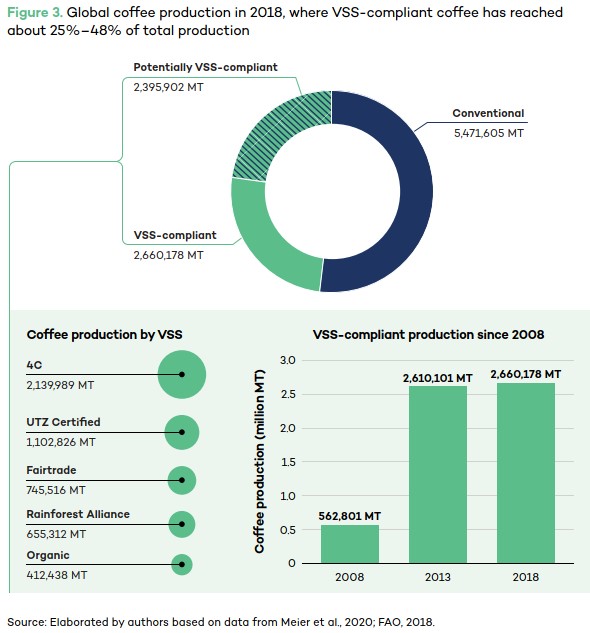

- Recent evidence suggests that the production volume of VSS-compliant coffee declined from 2018–2019 to just over 20% of total coffee production.

- Climate change adaptation is one of the main investment opportunities for VSS-compliant coffee, as it can enhance farmers’ access to technical assistance and finance. Investments in coffee plantations that adopt sustainable practices such as tree planting, water and soil conservation, mulching, and pest management can build resilience while improving yields and quality.

- The Rainforest Alliance’s forest carbon project in the Oaxaca region of Mexico aims to reforest the coffee plantations owned by 250 smallholder farmers to capture 130,000 tonnes of carbon dioxide emissions over 30 years.

- The eco.business Fund gives loans to financial institutions in coffee-growing countries for on-lending to coffee agribusinesses to obtain financial and environmental returns and build resilient plantations. Local financial institutions lend to coffee agribusinesses that are certified or adopt biodiversity and natural resource conservation measures aligned with the fund’s sustainability mandate. The fund also leverages blended finance from its partners (i.e., UK Aid Direct, Financierings-Maatschappij voor Ontwikkelingslanden, Kreditanstalt für Wiederaufbau) to provide technical assistance and training to its investees to build their capacity to adopt sustainable practices that protect biodiversity and promote sustainable natural resource management and climate adaptation.

- VSS-compliant coffee operations can lower investment risks by requiring more sustainable farming practices, secure buyer contracts, and better quality.

4. Cotton

- Cotton is grown on about 3% of agricultural land, of which more than half is irrigated. Most

cotton that is cultivated is genetically modified (64% in 2016) and of the Upland variety. - Smallholders in 70 countries, representing 99% of all cotton farmers worldwide, produce approximately 75% of all cotton.

- All central Asian countries and about 57% of African countries depend greatly on cotton exports for their economic growth.

- Some textile companies have lost brand value and profits by ignoring sustainability challenges, such as upholding decent working conditions and labour rights, in their supply chains.

- Cotton cultivation contributes about 0.3% to 1% of global greenhouse gas (GHG) emissions, which is probably considerably less than synthetic fibres, cotton’s main competitor in the textile sector.

- An estimated one third of global irrigated cotton is already or soon to be affected by soil salinization, which can lower productivity and cause soil erosion and degraded terrestrial and aquatic ecosystems.

- While cotton is grown on just 3% of the world’s agricultural land, its cultivation consumes approximately 6% of global pesticides affecting human and ecological health.

- GM cotton, designed with some pest-resistant properties, has not always resulted in lowering pesticide use, leading to pest resistance in some cases (i.e., the “superweed” Palmer amaranth)

- Cotton farmers can fall into vicious cycles of indebtedness as they must cope with decreasing and volatile cotton prices and increasing agricultural input costs hurting their profitability. This dynamic has led to rampant farmer suicides in the Indian cotton belt.

- The first Organic-certified cotton was produced in the early 1990s. Cotton compliance with the main VSSs operating in the sector—the Better Cotton Initiative (BCI), Cotton made in Africa (CmiA), Organic, and Fairtrade—has grown to more than 20% of global cotton production since then.

- VSSs require cotton producers to adopt more sustainable farming practices, which can include soil and water conservation, integrated pest management, and workers’ health and safety.

- An Egyptian organic cotton business reported that lower farm costs and improved average yields by almost 30%, along with better quality cotton, resulted in annual revenue increases of 14% from 2006 to 2011.

- Organic cotton can potentially lower GHG emissions by 46% and reduce water consumption by 91% compared to conventional cotton.

5. Palm Oil

- Plantations typically need to be replanted after 25 years to maintain productivity. Oil palm is the highest-yielding oilseed among all vegetable oils, accounting for 36% of all vegetable oil on only 6% of the land allocated for vegetable oil production.

- Palm oil became popular after trans-fats were banned in some countries and the WHO recommended limiting trans-fat intake, but its nutritional properties are still contested due to its comparatively high saturated fat content.

- Global demand for edible oils is expected to quadruple by 2050, and palm oil has the potential to meet around 60% of this demand.

- Asian countries are the largest importers of palm oil, led by India (USD 5 billion) and China (USD 4.6 billion). The EU and the United States consume only 15% and 3.5%, respectively, of the total palm oil production.

- Deforestation associated with palm oil is a major concern, as around 18 million hectares of tropical forests have been cleared for palm oil production. (...) Deforestation in Southeast Asia, Central Africa, and Western Africa and the destruction of peatlands associated with oil palm plantations are also major sources of GHG emissions.

- Demand for VSS-compliant palm oil has risen in the last decade, led by Europe and then North America. Cargill, Wilmar International, Nestlé, and Unilever have established sustainable sourcing commitments for palm oil.

- Many investment banks and asset management companies have integrated the NDPE (No Deforestation, No Peat, No Exploitation) and the RSPO (Roundtable on Sustainable Palm Oil) as part of their palm oil supply chain policy.

- Fifty-six FSPs representing about USD 7,900 billion in assets under management signed a statement in 2018 encouraging their investees in the palm oil sector to commit to full traceability of palm oil to the plantation level and to report regularly on their progress toward these commitments.

- Investments are required for palm operations to become VSS compliant in terms of covering certification and audit costs, such as conducting high conservation value and environmental impact assessments.

- Long-term financing is required to replace oil palm trees that are no longer productive and to cover the 3- to 10-year production gap until palms start producing fruit.

- VSS-compliant palm oil investments in sub-Saharan Africa could provide important development benefit potential due to the region’s need for food security and employment creation while avoiding deforestation and labour rights infringements.

6. Soybeans

- The development of varieties adapted to tropical climates and herbicide resistance through genetic modification has fostered the expansion of soy cultivation.

- Soybean-based meat substitutes, marketed by the food and fast-food industry, may signal a shift away from meat-based consumption that could lower demand for soybean-based feed but boost demand for higher-quality non-GM soybean inputs.

- China is the largest importer of soybean feed, accounting for almost 69% of global imports in 2020, followed by Europe.

- Significant productivity losses are expected in Brazil, while milder losses are being projected for Argentina, Bolivia, Colombia, and Uruguay, highlighting the need to adopt more aggressive climate mitigation and adaptation efforts in the sector, such as preventing deforestation and adopting longer-cycle varieties and irrigation.

- Soy farmers apply almost 35% of all pesticides used in Brazil. This is partly due to glyphosate-resistant GM soybeans, which make up 80% of total soybean production destined for animal feed

- The sustainability challenges associated with soybean cultivation prompted the establishment of VSSs in the sector. Organic soybeans have been produced since the 1970s, while the ProTerra Foundation (PTF) and the Roundtable for Responsible Soy (RTRS) started operating in 2006.

- China, the biggest soybean market, still consumes relatively few VSS-compliant soybeans. The slow uptake in VSS-compliant soybeans may be due to preferences for company-led sustainability schemes—such as Cargill’s Triple S, Amaggi’s Responsible Soy Standard, and Bunge’s Pro-S—among the largest soybean trading companies.

- A sizable portion of soybeans is consumed indirectly in the form of meat, poultry, and fish products, consumers are simply not aware of feed composition.

- There is certainly a need for a wide range of investments to help agribusinesses adopt and maintain VSS compliance measures.

- Among the top 10 VSS-compliant soybean countries, Togo is the only country with low indices, where investments may be riskier but where the development potential may be higher.

- Blended finance may be required to support the adoption of sustainable soybean cultivation practices, especially in low-income communities.

7. Sugarcane

- Grown in tropical environments, sugarcane has very high photosynthetic efficiency. But

sugarcane is a thirsty crop, requiring 1,500 mm to 2,000 mm of water per hectare annually or irrigation systems to maintain productivity, which can put pressure on local water resources and lead to conflict between water users.31 Sugarcane production can also pollute water bodies via fertilizer and pesticide runoff and sugarcane milling wastewater, which has led to ecological decline in many parts of the world. - It has become an important feedstock for producing food and fuel and is used to produce more than 80% of the world’s sugar

- Sugarcane cultivation and processing provide livelihoods for 100 million people across the world. The industry employs more than 1 million people in Brazil—nearly 25% of its rural workforce. The Thai sugarcane supply chain employs 1.5 million people, including 107,000 smallholders, and around 500,000 people in South Africa depend on the industry for their livelihoods.

- The controversial practice of burning sugarcane plantations before harvesting is still common in many regions.

- About 75% of this sugar is used to sweeten foods and beverages, and the remaining 25% is used for biofuels and industrial products.

- Brazil and India are the leading producers of cane sugar, with 39% and 20% of the world production, respectively, followed by Thailand, China, Pakistan, and Mexico.

- Developing countries account for approximately three quarters of global sugar consumption and are expected to have more demand in the coming years with increasing consumption of caloric sweeteners, processed products, sugar-rich confectionery, and soft drinks.

- Demand for sugarcane is expected to escalate as bioethanol demand grows. This demand is prevalent in Brazil, where about 60% of its sugarcane production was mostly destined for domestic ethanol production and consumption in 2014/2015.

- The production of sugarcane bioethanol is under scrutiny, however, as it competes for agricultural land with food products. Despite these debated issues, sugarcane is preferred as a bioethanol feedstock over other starch crops, such as corn, because of its high efficiency and development potential for Caribbean and African countries.

- Land grabbing associated with the expansion of sugarcane has been reported in Brazil, Sierra Leone, Indonesia, Kenya, Zambia, Mali, and Cambodia.

- Large cane sugar-consuming companies, such as Coca-Cola, Pepsico, Nestlé, and Unilever, have adopted sustainable sourcing commitments to meet increasing consumer demands for more sustainable sugar.

- Investments are particularly needed in infrastructure such as drip irrigation equipment, as well as to improve existing mills and build new ones, which typically have 4- to 7-year payback periods.

- Furthermore, there is considerable potential to scale up the production of sustainable bioenergy from sugarcane in some southern African countries, which have sugarcane industries that can be a source of sustainable heat, power, and biofuels.

- The development of new sugarcane-based materials, such as bioplastics, offers investment opportunities for venture capitalists. For instance, companies in the fashion sector are seeking to replace plastic made with fossil fuels with natural products. Research is ongoing to develop the technology needed to extract substances from sugarcane to replace highly polluting plastic and rubber. Amyris and Chanel are working with sustainably produced sugarcane to develop more sustainable products and materials.

- Proparco, the investment arm of the Agence Française de Développement, gave Bonsucro-certified Acucar Guarani in Brazil a USD 50 million loan to improve its sugarcane ethanol processing facilities.

- African Development Bank, the Agence Française de Développement, and the United Nations Environment Programme (UNEP) are working to create favourable conditions for private investments in support of sustainable development in the sugarcane sector.

Tea

- Tea is one of the most consumed and traded beverages in the world, offering appealing flavours to a broad range of consumers. It originates from processing the young leaves of the Camellia sinensis bush, which has a productive lifespan of 40–100 years.

- More than 2,000 leaves, processed within six hours of being harvested, are needed to make half a kilogram of tea. This processing requirement has shaped the industry, which has evolved toward a vertically integrated value chain reliant on closely located tea cultivation and processing facilities and intensive labour.

- Some 13 million people, of whom 9 million are smallholders, depend on tea production for their livelihoods.

- Production is highly concentrated, with China, India, Sri Lanka, and Kenya producing about half of the world’s tea.

- Studies in countries such as China and India have found high residue levels of banned substances in tea production areas (e.g., DDT, methomyl, endosulfan) and pesticide residues in final products.

- The excessive misuse of pesticides can imperil tea workers and consumer health, and this could pose reputational and market risks to investors.

- Tea is grown in areas of high biodiversity and has historically been associated with the removal of tropical forests for tea cultivation and drying. Cultivated in monoculture plantations, tea contributes to habitat loss and is linked with the decline of endangered species such as India’s lion-tailed macaque and Sri Lanka’s Horton Plains slender loris.

- Demand for VSS-compliant tea is expected to continue growing in traditional markets, mainly Europe and North America.

- Increasing demand for organic tea appears to be related to its health benefits and lifestyle changes that favour ready-to-drink tea, where major beverage companies such as Coca-Cola have a stake.

- Consumption of VSS-compliant tea is expected to grow in the middle class in China, India,

Indonesia, and Sri Lanka, as well as in Rwanda, Uganda, and Kenya. - The Jalinga Tea Estate, located in the province of Assam in India, grows Organic and Fairtrade tea for export. (...) It has become the first carbon-neutral certified tea estate in the world as it applies climate-smart practices, such as shifting from using coal to solar energy to process tea leaves and conserving forests, which have contributed to the estate’s profitability.

- SORWATHE, a Rwandan Organic- and Fairtrade-certified tea company, introduced kindergartens in its plantations with the assistance of UNICEF, which increased productivity among mothers by 5 kg to 20 kg of tea harvested per day.

- The Rainforest Alliance and IKEA Foundation partnership support smallholder Kenyan tea growers to consume locally produced no-smoke briquettes, which preserves more than 80,000 trees by reducing firewood consumption in tea factories by 30% while also reducing tea-drying energy costs.

- Blended finance along with blockchain technology is being used to provide VSS compliance assurances in real time (i.e., the origin of tea and land titles) while offering favourable lending conditions to Malawian growers supplying tea to Unilever and Sainsbury.

Conclusions and recommendations

- The agricultural sector remains an important driver of climate change, deforestation, biodiversity loss, water appropriation, and ecosystem pollution, as it uses 38% of the world’s land, 70% of fresh water, and large amounts of agrochemicals.

- For the most part, VSS-compliant production in the eight agricultural commodities examined is growing faster than conventional production. With the exception of bananas, soybeans, and sugarcane, VSS-compliant production represents more than 10% of global production within the sectors examined.

- Blended finance models that share risk between public and private stakeholders offer great promise to mobilize desperately needed financial resources to increase agricultural production while enhancing the ecosystems and supporting the communities that underpin agriculture.

- VSSs offer promising avenues to increase investment in sustainable agriculture in developing countries. They can also enable agricultural producers to access finance to support their business development while improving their social and environmental performance.

- The VSS have the potential to help FSPs reduce financial risks and strengthen farmers’ bankability while enhancing their impact.

Since 2020, the Alliance of Bioversity International and CIAT have been investigating new business

models to connect scientific products to markets – and create demand – by liaising with the actors

operating in the innovation ecosystem. Building on CGIAR’s legacy of research and innovation, and

with initial funding from the Italian Ministry of Foreign Affairs, the Alliance launched A4IP in 2021 as

a ‘venture space’ aiming to bring science and entrepreneurship together to co-design disruptive

technologies at the nexus of agriculture, environment and nutrition.

- In 2021, A4IP engaged in several activities, including the global Agrobiodiversity Innovation Challenge, which received 350 submissions involving 1,050 start-ups representing 76 countries.

- A4IP also organized the Agri-Food Tech Innovation Forum in November 2021 on ‘The Role of Venture Capital in Agricultural and Food Systems: Creating Opportunities and Scaling Up Science-Based Innovations,’ supported by many companies, foundations and donors, attracting an audience of 1,100 participants.

· Tiffany Talsma, Climate Strategy Specialist, CGIAR

· Arko Chatterjee, Founder and CEO, NaturaYuva

· Hans Hoogeveen, Independent Chairperson of the FAO Council,, Food and Agriculture Organization of the UN

· Francesca Nugnes, Expert on SME Impact Finance, Consultant, International Institute for Sustainable Development

· Vivek Voora, Senior Associate, International Institute for Sustainable Development - State of Sustainability Initiatives review: Standards and investments in sustainable agriculture

See recording @34:40 Event Recordings — International Agrobiodiversity Congress (eatgrowsave.org)

No comments:

Post a Comment